We all have heard different ads saying “Mutual Fund Sahi hai” which means the mutual fund is the right thing to do, Is it correct? What is actually a Mutual Fund? What are the different types of mutual funds? How can we invest in Mutual Funds? Are there any tax benefits for investing in Mutual funds? Yes, we know there will be a lot of doubts and thoughts on your mind. Let’s discuss mutual funds today in the best possible way we could.

There is a conventional misconception that mutual funds are share market-linked products and they invest the money only in equity, which is totally wrong. Not all mutual funds are Equity market related, some of them invest in the Share market, but there are a lot of mutual funds which invest only in fixed income assets like gold, Govt bonds, and securities, Debentures, real estate, debt funds, Treasury bills, etc. Nonequity related Mutual funds offer the safest investment options capable of giving good returns and anyone could consider it, as the returns promised by such funds are higher than regular bank FD and they provide high safety of capital as well. We’ll discuss the types of mutual funds later, but first of all what are mutual funds?

Let me explain it with an example: imagine you want to invest thousand rupees ( Assume you are planning to Invest in the Stock Market) from your savings every month and there are three ways to plan and select stock for investment. The first option is where you do a fundamental analysis on different stocks from various sectors and find out the best stock which can give you good returns. It requires some really good talent and time to do such an analysis on multiple stocks, picking the right stock is like an art and if you have that skill and time you can do it. The second option is to consult a financial advisor who will recommend different stocks and you can invest in those stocks directly by giving a fee to the advisor.

There are certain drawbacks with these two methods, If you are someone who is capable of choosing stocks by yourself, then you have to keep up with the latest news and updates about the companies you have invested in, Changes in the Govt Policies which can affect these stocks, Analyze the financial position and performance of the Company, and read their quarterly and annual report to make sure the numbers are up to your expectations, etc. You have to pay a certain amount as a fee to the advisor every month or at the time of investment, if you have decided to get stock pick advice from a SEBI registered advisor. Another issue with the above two methods could be the cost of some stocks, just like MRF and Shree Cement which are trading above Rs. 25,000/- per Single share, which couldn’t be purchased with your Rs. 1000/- capital.

Just as a solution to all these hassles, here comes the third option of Investing via a suitable Mutual fund scheme of your choice. If you invest money in a Mutual Fund scheme, then you don’t have to do all these hectic Fundamental analysis periodically, run through stock-specific news and Policies daily, tracking the market and foreign exchanges periodically, and all such sort of stuff. The Fund house will track all these things and perform in-depth research for its investors thereby saving a lot of your valuable time. Also, you don’t need to worry about the huge share prices of Stocks, the fund house is capable of buying any stock and they will issue it to you in accordance with your investment amount.

What Is a Mutual Fund and How does it Function??

Mutual Fund Schemes are Investment options where you could invest your money in Equity, Debt, or on Special Assets as per your choice, wherein the investment is professionally managed and maintained by Mutual Fund Houses which promise you a good return of Investment and flexible investment horizon.

Mutual funds pool huge capital from multiple investors by promising good returns on their investment from multiple investors, like you and me. The Mutual Fund Houses offer multiple investment opportunities like investing in Equity related Products, Debt instruments, or a combination of both. The investor has full power to choose which mutual fund Investment type / Scheme he likes to invest his money. The Mutual fund house invests this pool of money into a basket of carefully Picked Equity / Debt products and issues “Mutual Fund Units” equivalent to the investment amount to every investor. Mutual Fund Units or simply Units are the base quantity of a Mutual Fund scheme, In the share market, we purchase shares, like in Mutual funds we purchase Mutual fund Units. Mutual Fund Units like shares are stored in our Demat account.

We would like to take a pause here and take you a bit in detail to the Mutual Fund Industry, to give you a better understanding and Clarity about the industry structure and Functioning. We have used the Words Mutual Fund Houses, Mutual Fund Schemes, Mutual Fund previously and if you are confused about these terms, better suggest to read the following section where we briefly describe the Mutual Fund Industry structure.

We know that we can set up a company in India as per the Companies act of India. You may think that Mutual Fund Houses, like HDFC Mutual Fund, Axis Mutual Fund, SBI Mutual Fund, are companies set up as per the Companies act, But No !!! Mutual Fund Houses (Mutual Fund) are not companies they are Trusts, They are established and Operated as per the Indian Trusts Act. The Mutual Fund Houses are Set up by a group of people or institutions and they are called “Sponsors” of the Trust. Sponsors appoint either a company or person to look after the whole Mutual Fund Activities and he is called “Trustee”. The trustee then appoints Asset Management Companies (AMC) to manage the day-to-day activities of the Mutual Fund and the pool of investor money. The trustee also appoints “Custodian” to look after the securities invested by AMC. AMC Appoints Registrar and Transfer Agents (RTA) to maintain a record of the securities handled by AMC and facilitate the transfer of Mutual fund Units to Investors and keep a record of all Investor activities. Eg. HDFC Mutual Fund is a Trust Sponsored by HDFC & Standard Life Investment Ltd, with HDFC AMC as Asset Management Company and HDFC Bank as Custodian along with Various RTA like Karvy Fintech Ltd.

The Mutual Fund Houses will have multiple investment options called Mutual Fund Scheme, Each Mutual Fund Scheme will have an Asset Manager / Fund Manager assigned to the scheme by AMC. The role of the Fund Manager is to carry out in-depth research on various investment opportunities available, to invest the Pool of money he handles to make good returns over time. The performance of Mutual Fund schemes are directly dependent on the efficiency and skills of the Fund Manager, because he has to identify the right opportunity and invest on right time to generate maximum returns. That is the reason why the same category of Mutual Fund scheme of different Fund House gives different Percentage of Returns, like Large-cap Fund of Axis Mutual Fund will be giving X% Returns whereas are Large Cap Fund of SBI Mutual Fund will be giving Y% Returns.

One important thing every investor should keep in mind while Opting to Invest in Mutual Fund is that here the Investor cannot decide the Specific Company stocks or Debentures from a specific company or Specific Govt Bond to Invest his money, It’s the Fund Manager who decides where to invest the pool of Money exactly and on what percentage he should invest the money on multiple securities. The Fund Houses will offer investors various schemes like Large Cap Fund, which invest in the Large Cap companies on Nifty but you can’t say you need to invest the whole money only in HDFC Bank and Reliance while choosing that scheme, the Fund Manager is the one who decides to select the Large-cap Stocks to invest in deciding in the percentage of allocation as well based on his research. Similarly, there are multiple Schemes offered by Fund Houses like Mid Cap Fund, Small Cap Fund, Hybrid Fund, ELSS, Overnight Fund Etc. The Investor can choose which scheme as per his risk appetite and returns perspective, the Fund Manager will be the one deciding which specific securities to invest based on the Scheme the investor has chosen.

In short, the Allocation of capital is based on the mutual fund managers. Some managers keep a certain percentage of money invested and keep a certain percentage of the money with them to invest when the market crashes. Advantages of mutual funds include diversification, Exposure to good companies with a smaller amount invested and your money is managed by experts who are continuously tracking the portfolio for better returns.

Now we believe that you have got a good understanding of How a Mutual Fund House Function and the Various Intermediaries involved in the Business.

Association of Mutual Funds in India (AMFI)

We know the importance of a Regulator in any business environment. We know SEBI as the regulator of the Secondary Market / Stock Market of Our Country. Similarly, AMFI is the regulator for the Mutual Fund Houses business, which ensures all the Fund Houses carry their business in an ethical manner as per the rules, regulations, and standards of the industry and ensure the protection of the Investors money. AMFI is not a completely independent regulator for the industry, because Fund houses invest in Stock Market so SEBI Comes into the Picture, Fund Houses invest in Govt Securities so RBI Comes into Power, They invest in Gold and Real Estate, etc then Governing laws and legislative Controls should be respected. So as an informed investor AMFI Should be our primary focal point to approach in case of any disputes with the Fund House.

Entry and Exit Load on Mutual Fund Schemes

In the early days, we had to pay a certain amount as Fee in order to Join a Mutual Fund Scheme, In August 2009 SEBI had waved off the Entry Load on Mutual Funds to promote the Mutual Fund Industry and Investment Options to the Public. So thanks to SEBI, Now we don’t have to pay any Fees to Join any Mutual Fund Scheme.

But there is an Exit load on the Mutual Funds scheme even today. When we join a Mutual Fund Scheme the investor has to mention the period till when he needs to keep his money Invested. So every Investor before joining a Mutual Fund Scheme has to decide his investment horizon on the Scheme but nowadays Applications like Groww or Zerodha coin will allow you to select and start investing in any mutual funds without defining a time period Initially. Mutual Fund Houses Offers schemes having investment horizons from 1 Day to 10 / 20 years or more. A premature exit or withdrawal from the Scheme will attract an Exit Load on the Investor. The Exit Load will be a small percentage value of his Investment and the % Rate will be clearly indicated on the Scheme Information Document. The majority of the Fund House does not charge Exit load after 1 continuous year of Investment.

Scheme Information Document (SID)

This is a must-read document by all Mutual Fund Investors. Every Mutual Fund Schemes have a unique SID. The SID will detail out all the relevant details about the Mutual Fund Scheme. It will show the type of the Scheme (Large Cap, Mid Cap, ELSS, Tax Saver), the Assets and Securities on which that Fund Scheme Invest. Details of the Fund Manager, AMC, Custodian, RTA, Fund House, Period of Inception of the Fund, Exit Loads % and Criteria, Expense Ratio, Fund Management Charges, Nomination requirement, Past Performance of the Fund, Total Fund Value as of Specific Date, Benchmark for the Fund, Mutual Fund Unit Price, Minimum Investment Value, Investment Horizon, specific terms and conditions and so on. So all the relevant information about a Mutual Fund Scheme will be published on that SID, and an Informed and Intelligent investor must read it before investing in the Mutual Fund. The SID is revised periodically to reflect the most accurate information and data.

Benchmark for Mutual Fund Scheme

Benchmark is just a reference used to compare the performance of the Mutual Fund Scheme, a Mutual Fund scheme will have one or more benchmarks to Compare its periodic performance and it will be defined in Scheme Information Document.

Suppose if we invest in Large Cap Funds we can see from our portfolio that our investment is giving 15% returns, you can be happy by seeing the return on Investment. But wait, what if Nifty50 has grown 20% in the same period? Now you may be sad because your Mutual Fund scheme could not even perform as well as Nifty50, you would have thought for a moment that it would have been better to invest in Nifty50 rather than on the Mutual Fund Scheme as it has given Higher returns. So in this example, we have taken Nifty50 as a Benchmark to compare the Mutual Fund Performance.

So we must note the Benchmark of the Mutual Fund Scheme prior to Joining it and Compare its performance with the benchmark. SID will be showing the past performance of the Fund for your understanding. Suppose if your Mutual Fund could not beat the Benchmark over multiple periodic years, then it shows poor management of the Fund Manager, and you should consider exiting from the scheme to find better opportunities.

Various Mutual Fund Schemes have their own Scheme characteristics related to Benchmark for Performance comparison and investors should compare it periodically to ensure better performance of their investment.

Expense Ratio and Portfolio Turnover Ratio

The Expense Ratio of a Mutual Fund is the Percentage of Charges levied on the investor by the Mutual Fund House for Managing his assets. We know that it’s the responsibility of the AMC and Fund Managers to manage the pool of money collected from investors efficiently to give better returns. Mutual Fund Houses require capital to run the business and provide better service to its customers, Fund Houses collect a charge or deduct a percentage of the profit from the investor to meet its day-to-day expenses. This percentage of charge collected from the investor is represented by the Expense ratio.

It’s worth noting that the Expense ratio varies from Fund Houses to Fund houses and varies according to Mutual Fund Schemes. Some Mutual Fund schemes will have a higher Expense ratio and some will have a lower expense ratio. This information will also be given in SID. So investors are advised to compare the expense ratio of Multiple Funds and choose the one having a minimum Expense ratio. It should be noted that certain types of mutual funds require continuous monitoring and a high level of effort from the Fund Manager, such mutual fund schemes will definitely have a higher expense ratio, but they might be giving higher returns also. So do not fall directly for a low expense ratio other parameters should also be taken into account while choosing a Mutual Fund Scheme.

A Mutual Fund Scheme will have specific securities allocated to it based on Fund Managers research and analysis, if the Fund Manager Feels that certain assets or securities on the Mutual Fund Portfolio are not performing as per his expectation he will remove that asset and compensate it with better assets or securities. The Portfolio Turnover ratio shows the number of times the Fund Manager has completely reshuffled the assets or securities on the Mutual Fund Portfolio. A Portfolio Turnover ratio of 2 or 3 in a year is okay, but a higher portfolio ratio shows poor analysis from the Fund Manager and his lack of confidence on the asset class performance, which is not a good sign for a Mutual Fund Scheme.

Assets Under Management (AUM) & Net Asset Value (NAV) of Mutual Fund

The Assets Under Management (AUM) shows the total capital amount invested by all investors on a particular Mutual Fund Scheme. A Fund Manager will have to Manage capital and invest them on the right investment opportunities to give better returns for the investors. A Higher AUM on a mutual fund scheme shows higher confidence of the Public in the Scheme and also since the scheme has a high AUM the amount of money collected from individual investors to meet the Fund House Expenses, ie Expense Ratio, will be lower.

Net Asset Value (NAV) of a Mutual fund is the current market price of one unit of the Mutual Fund. Unlike Shares, Mutual Fund Unit’s price value, ie NAV, does not change every second. NAV Changes only on a daily time frame and is Published every day by AMFI. NAV shows how much money we will get when we sell one unit of Mutual funds at that time.

The Exit Load of a Mutual Fund Scheme will be calculated as a certain percentage value of the NAV. The Exit Load Percentage of deduction will be given in Scheme Information Document.

TYPES OF MUTUAL FUNDS

What are different types of mutual funds? There are a large number of Mutual Fund Schemes available and provided by Multiple Mutual Fund Houses, it’s really difficult to effectively classify and group them. But here we will try to Group and Classify various Mutual Fund Schemes in the best possible way we could. It’s going to be really interesting as well as an intricate section of this chapter, hope you guys could catch up and gain valuable information.

Broadly classifying, all types of mutual fund will either invest in equity or debt or a mix of both, Still, it can be divided into open-ended and close-ended mutual fund schemes.

Open-ended funds

In an open-ended mutual fund, an investor can invest or enter and redeem or exit at any point of time. It does not have a fixed maturity period. Capital won’t be blocked for a certain amount of time.

Close-ended funds

Close-ended mutual funds have a fixed maturity date. An investor can only invest or enter in these types of schemes during the initial period known as the New Fund Offer or NFO period. His/her investment will automatically be redeemed on the maturity date. They are listed on the stock exchange(s).

Let’s take a look at the various types of equity and debt mutual funds available in India:

Kudos…!!! Now you have a better understanding of the General Terms as well as General Classification of the Mutual Fund Scheme owing to multiple criteria if you went seriously through the previous section. You might have realized that the major asset class the mutual funds invest in are Equity and Debt Instruments. So let’s get deep into them and try to understand various types of Debt and Equity Mutual Funds Schemes available in India and decide which would be the best for you.

EQUITY MUTUAL FUNDS

These types of Mutual Fund Schemes invest in the various company shares which are listed on the Secondary market. These are one of the most popular mutual fund schemes. They allow investors to participate in stock markets with passive efforts. Though categorized as high risk, these schemes also have a high return potential in the long run. They are ideal for investors in their prime earning stage, looking to build a portfolio that gives them superior returns over the long-term. Normally an equity fund or diversified equity fund as it is commonly called invests over a range of sectors to distribute the risk.

As said Equity oriented Mutual Funds being the one which offers highest returns, as per historical data, we being an Intelligent Investors should possess good understanding on the same. So let’s move ahead and learn more about the types of Equity Mutual Funds in our Market.

One Important point to be noted is that a Mutual Fund House is allowed to have only a single scheme in the subcategory. For Example Axis mutual fund can have only one scheme in the Large-cap Equity fund category, it can’t have multiple large-cap fund schemes. This allows the investors to avoid confusion and facilitate easier Fund Selection as per their wish.

Large Cap / Blue Chip Fund

In these types of Fund Minimum 80% of on Investor money should be invested in Large Cap Companies listed on the Stock Market. These Funds usually provide better and consistent returns and possess low risk as the investment is made on the top companies of the nation, whose chance of underperformance is comparatively very low. As the dependence or role of Fund Manager is limited, these Funds comparatively have a lower expense ratio.

Mid Cap Fund

In these types of Mutual Funds, a Minimum 65% of the Investor’s money should be Invested in Mid Cap Stocks listed on exchanges, the rest of the asset allocation is as per the Fund Managers’ expertise. Here the dependence on the Fund Manager is a bit higher as he has to choose the best performing Mid Cap Stocks and needs to have a close watch on the same. So the risk is a shade higher for Mid Cap Funds compared to Large Cap Funds because Mid Cap Companies are severely hit in case of any crisis or change in Govt Policies. Good Mid Cap Funds usually provide better returns than Large Cap Funds.

Small Cap Fund

In Such types of Funds, a Minimum 65% of the Investors money should be allocated to Small-Cap Stocks listed on the Secondary Market. Good Small Cap companies with better business can give the highest returns and can have sudden profit jumps if their products are of great demand and value. At the same time, these Funds carry the highest risk on Equity-based Funds as small-cap companies get the most affected or even completely shut off in case of crisis. So the dependence on the Fund Manager is really high and he has to pick the best small-cap companies with great upside potential to invest and need to perform thorough study and research on them continuously. As the Fund Manager role is higher, Small Cap Funds have a higher expense ratio usually.

Multi-Cap Funds

Here the Fund Manager has to make a minimum 65% allocation in Equity Instruments, and there is no specific limit on the percentage allocation required on each Capital Sector. The Fund Manager can decide the percentage of allocation based on his investment plans and research. Since these funds have a higher dependence on the Fund Manager, the expense ratio is also high for them.

Focused Funds

These schemes wherein a maximum of 30 stocks are allowed in the Portfolio, which can be from various sectors as well as market capitalization, which the fund manager believes to provide better returns. The fund manager can decide the stocks to be part of the portfolio as per his studies and research. These funds usually invest in a mix of evergreen sectoral stocks.

Tax saving funds:

These funds offer tax benefits to investors. They invest in equities and are also called Equity Linked saving schemes(ELSS). These types of schemes have a 3 year lock-in period. The investments in the scheme are eligible for tax deduction u/s 80C of the Income-Tax Act, 1961. The fund invests 80-100% of its portfolio in equity or equity-related instruments. The equity strategy aims to provide long term capital appreciation from a reasonably diversified portfolio consisting of mid-cap and large-cap companies

Value or Conta Funds

A Mutual Fund House can either have a Value-Based Fund or a Contra Fund Only. Fund Houses are not allowed to provide both types of Plan, they could issue either Value or Contra Fund.

In a Value-based Fund, the Fund Manager invests in an Undervalued stock from a buzzing sector expecting better growth on it. Whereas in a Contra Fund the Fund Manager invests in Undervalued Stocks of a currently lower-performing sector expecting its better growth in the future as per his research. These types of schemes possess great risk and have a high dependence on Fund Managers as investments are made mostly on undervalued stocks, which may be adversely hit if market conditions change.

DEBT MUTUAL FUNDS

These types of Funds invest the major portion of the investor fund in Debt Instruments which gives fixed returns like Govt. Bonds, Company Debentures, Commercial Paper, Treasury Bills etc. Credit rating agencies provide ratings for Debt Instruments and those with high ratings will have good liquidity, safety and return on investment. Debt Mutual Funds are best suited for those who prefer to have higher returns safely and consistently and the best ones usually provide 9% to 13% returns, which is much better than regular bank Fixed Deposits.

One important aspect to be discussed about Debt Funds is that through Debt mutual Funds you can opt for an investment horizon from 1 Day to 7+ years or more. Experts often recommend to opt for Debt mutual funds usually if your investment horizon is upto 3 to 4 Years, anything above which also gives you consistent returns, but it’s seen that on a long term Equity Funds have outperformed Debt Mutual Funds.

Just reminding that as we discussed in Equity Funds a Mutual Fund House is allowed to have only one scheme in the Debt Fund Sub Categories.So let’s Get to know a glimpse of various types of Debt Mutual Fund in our market,

Investment Horizon from 1 Day to 1 Year

For those investors who could invest only for a short duration, ie 1 day to 1 year could consider choosing Debt Mutual Funds which provide pretty decent returns like Overnight Fund, Liquid Fund, Ultra short term Fund, Low Duration Fund and Money Market Fund. All these Funds invest mainly in Treasury Bills, Short term CD, REPO, Commercial Paper etc and provide highest safety for your investment with good liquidity. Since these Funds are intended for small investment horizons most of these Mutual Fund Schemes don’t charge exit load after 7 days. Overnight Funds are the one suited for the lowest investment duration like upto 1 week and Money Market Funds are the one suitable for investment close to 1 year respectively based on the returns and investment duration respectively.

Overnight Funds

These are Funds provide the opportunity to invest with the lowest investment horizon in debt instruments, some of them even have a maturity date of 1 Day. They usually don’t charge an exit load after 2 days and are best suited for ultra short term (2 Days to 2 weeks) investments rather than keeping money idle in savings accounts.

Liquid Funds

These Funds are suitable for an Investment horizon of up to 3 months, majority of the funds does not charge exit load after 7 Days and gives returns of 4% – 6% Usually. These funds mainly invest in Treasury bills of Govt.

Ultra Short term Debt Funds

These types of Mutual funds are suitable for investment horizon for 3 to 6 Months and provide 5% -7% returns usually. They also mainly invest in T- Bills and commercial papers for a short duration.

Low Duration Fund

These types of Debt Mutual Funds are suitable for Investment horizons of 6 to 12 Months and provide returns of 7% -9 % usually. The majority of the Funds do not charge premature exit loads, but a few do. These funds invest mostly in T-Bills, Commercial Papers, Short term Deposits etc.

Money Market Funds

These Debt Mutual Funds are suitable for investment till 1 year and usually provide returns of 6% -9%. Most of the Funds do not charge premature exit loads and they mainly invest in T-bills, CDs, REPO etc.

Investment Horizon from 1 Year to 3 Year

Short Duration Funds

These Funds are suitable for investment spanning from 1 to 3 Years and usually provide returns of 9 % to 12%. These types of Funds mainly invest in Corporate Bonds and Debentures of maturity spanning from 1 year to 3 years. Exit loads are charged on these types of funds if redeemed within 6 months.

Floater Funds

As per SEBI Norms minimum 65% of the Assets Under Management (AUM) has to be invested in Floating rate debt instruments. These types of Debt funds usually provide 9% -11% returns on an investment horizon of 1 year to 3 years. These funds have a high credit risk due to investment in floating rate debt instruments.

Banking and PSU Debt Funds

As per SEBI norms, these funds have to invest 80% of the AUM on Debt instruments issued by PSU, Banks, and Public Financial Institutions. These funds usually provide returns between 10% -12% for an investment of 1 year to 3 years. These funds provide better safety of investment as they invest in Public Sector Company Debt instruments whose probability of default is negligible.

Investment Horizon from 3 Year to 7+ Years

Medium Duration Funds

These funds mainly invest in Govt Securities, Corporate Bonds, and Debentures of maturity between 3 Years to 7 Years. These are medium risk category debt funds which provide a return of usually 9% to 11% for investment above 3 Years usually.

Long Duration Funds

These funds mainly invest in Govt Securities, Corporate Bonds, and Debentures of maturity of more than 7 Years. These funds possess a slightly higher risk owing to the long duration of investment as the Bond rate is subjected to changes during such a high tenure. Usually, these types of Funds provide returns of 10% to 11%.

Dynamic Bond Funds

These types of Debt Mutual Funds invest in Debt instruments of any maturity period and the choice of the debt instrument to invest is completely entitled to the Fund Manager. These funds usually provide returns of 11% to 13%, but have a slightly higher expense ratio and medium risk owing to complete dependence on the Fund Manager.

Corporate Bond Funds

These types of Funds have to invest a minimum 80% of AUM on AAA-rated Corporate Bonds of any duration. These are medium risk category debt funds which usually provide 11% to 13% returns.

Credit Risk Funds

These funds have to invest a minimum 60% of AUM on AA and A-rated Corporate Bonds together. These funds usually provide returns of 8% to 10% but are considered as a high-risk category of debt funds due to investment in AA and A-rated Bonds.

Gilt Funds

These Funds have to invest a minimum of 80% of AUM in Govt. Securities. They are preferred by investors who are risk-averse and want no credit risk associated with their investment. These funds usually provide returns of 11% to 13% and are considered to be the utmost safe type of Debt Fund as the majority of Funds are invested in Govt Securities. These funds possess a slight interest risk as the Govt Securities interest may change from time to time.

Risk Types in Debt Mutual Funds

There are mainly three types of risk associated with Debts funds,

- Credit Risk

It refers to the risk scenario, where the issuer is not repaying the principal and interest of the debt instruments. Such risk is mainly seen on low-rated Corporate Bonds and Debentures.

- Interest Rate Risk

It indicates the risks associated with periodic changes on the debt instrument interest rate.

- Liquidity Risk

It indicates the risk carried by the fund house of not having adequate liquidity to meet redemption requests of the mutual fund due to low participants in the scheme or any such similar reasons.

HYBRID MUTUAL FUND

Whola…!!! Now you have learned and got a better understanding about the Equity and Debt type mutual funds and their subtypes in detail from our previous chapters. We are quite confident that previous chapters on Mutual Fund have given you a much better and clear understanding about the Mutual Funds.

As we have told you earlier Debt Mutual Funds are suitable for risk-averse persons who wish to grow their wealth consistently with maximum safety. Whereas Equity mutual funds are suitable for those who want to grow their wealth a bit more aggressively and in a fast paced manner by taking that extra risk stock market has inherently. But wait a moment, there can be one another category of people, like those in their middle ages, who are willing to take a few calculated risks by investing 50% in Equity Products and 50% in Debt instruments. By doing so they could enjoy the benefits of quick growth in the Equity market and the Safe and consistent wealth growth of Debt instruments too. To cater the needs of such a category of people HYBRID Mutual Funds were introduced, which invest a percentage of AUM in both Equity and Debt Market Instruments.

So without further ado let’s get to know Hybrid Mutual Funds types in detail.

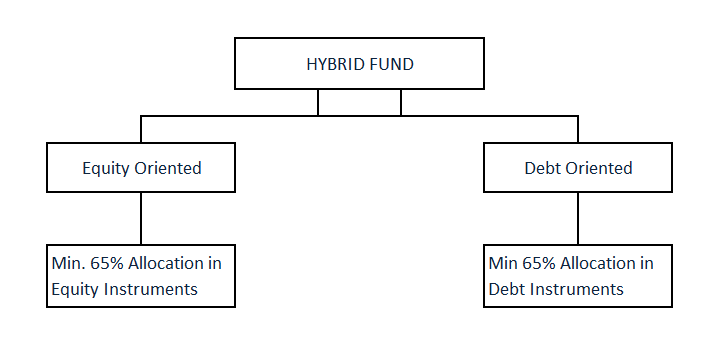

Hybrid Mutual Funds or Hybrid Funds can be broadly classified into 2 Categories as Equity Oriented Hybrid Fund or as Debt Oriented Hybrid Fund based on whether Equity or Debt products get maximum asset allocation on the Fund.

In Equity Oriented Hybrid Funds a Minimum of 65% of AUM is allocated for Equity Instruments in the Mutual Fund portfolio, whereas in a Debt oriented Hybrid Fund Minimum 65% AUM allocation is provided for investment on Debt instruments.

Let’s discuss the major types of Hybrid Funds available in our market currently,

Conservative Hybrid Fund

These types of Hybrid Funds have maximum asset allocation in Debt instruments. Such Funds should invest 75% to 90% of the AUM in Debt instruments and the remaining in Equity Market. Such Funds usually provide better returns of Investment horizon of more than 3 years.

Balanced & Aggressive Hybrid Funds

As per SEBI Norms, a Mutual Fund House can have only either a Balanced or Aggressive Hybrid Fund Scheme.

Balance Hybrid Funds 40% to 60% of total AUM in the Equity market and the rest in Debt Instruments, whereas an Aggressive Hybrid Fund invests 65% to 80% of the AUM in the Equity market and rests in Debt Market. Historic data suggests that the Aggressive funds have given higher returns compared to balanced Funds owing to their higher Equity market allocation in Fund Portfolio.

Dynamic Asset Allocation Fund

As the name suggests these mutual funds do not follow any strict percentage allocation on Debt and Equity Market, the Fund Manager can decide the allocation of Debt and Equity Instruments as per his research and studies. Sometimes the Equity allocation can go even up to 100% if the Fund manager finds that the Secondary market conditions are well suited to give higher returns with limited risk. As these funds have a higher dependence on the Fund Manager the expense ratio is usually a shade higher comparatively.

Multi-Asset Allocation Fund

As per SEBI regulations these Mutual Funds must invest in at least 3 asset classes with a minimum of 10% of AUM allocation on each asset class. These types of Mutual Funds provide better diversification due to multiple asset class allocation. The asset classes to be invested in can be Equity, Debt, Gold, REIT, etc. Such Funds usually provide better returns on an investment horizon above 5 years and it has higher dependence on the Fund Manager, as he has to periodically assess the economic conditions and invest accordingly in the best suitable asset class.

Arbitrage Funds

This type of Fund is one of the safest of all types of Mutual Funds whether it is Equity or Debt type. These funds make use of the principle of arbitration and are often said to be the type of mutual fund with 0 Downside or Capital risk. These types of funds have to invest a minimum of 65% of the AUM in the Equity market. These funds usually provide a return of 4% to 7% and make use of the volatility of the market to generate profits.

Equity Saving Fund

These types of Funds have to invest a minimum of 65% Equity market and 10% Minimum in the Debt Instruments. Since the percentage of allocation in the Equity market can go up to 90% as per Fund Manager’s decision, these types of Hybrid Funds possess a shade higher risks comparatively and behave more similar to an Equity Mutual Fund.

Selection of Right Mutual Fund for You

We have promised you earlier that we will try to make you capable of choosing the right mutual for you by yourself. We know the Direct and Regular types of Mutual Funds, the one purchased directly from Fund House and the other sold by Agents / Intermediaries respectively. Traditionally even though the regular type of Mutual Fund has a higher expense ratio, people often tend to go with the same due to a lack of proper knowledge and understanding about the Mutual Fund industry, various types of Mutual Funds, and the dilemma in the selection of the right Plan, Fund house, etc.

We at Fineracy are trying to build a Financially literate community capable of making intelligent financial decisions by themself. If you were with us completely throughout our Mutual Fund series, you know how a Mutual Fund Industry operates, Who are the Major Intermediaries supporting the Industry, the Regulator of Mutual Funds in India, Equity / Debt / Hybrid Mutual Funds, SID, Expense ratio, AUM, NAV, Exit Loads, Benchmark and Much more, which comes handy to help you choose the best Mutual Fund Scheme that suits your needs or goal.

We all know that Mutual Fund Plan or Simply Mutual Fund is a Financial Product that helps us to systematically grow our wealth. Before you try to figure out the best Mutual Fund available in the market, you better decide and fix the Plan or life goal or an event that you aim to achieve by investing in Mutual Fund. The aim can be to meet your retirement goals, to buy a house after 8 years, to meet your child’s higher education in 10 years, to buy a car in 2 years, to buy a laptop in 6 months, or to grow your wealth indefinitely overtime etc. The goal you plan to achieve can be anything, it’s completely dependent on you and it’s your dream and wishes you plan to achieve in a certain period.

So the first and foremost two important parameters you must be well aware of before deciding a mutual fund are the Amount of Money required to achieve your goal and the Time Period within which you plan to achieve that goal. These are the two key parameters that decide which Mutual Fund scheme you should opt and how much money you should start investing from today so that you can achieve the goal you set on time.

From the above parameter defined Time is completely your choice, but while deciding the Money required to meet your goal you should be a bit more conscious. Because if you plan to buy a house after 8 years in a city where the current market price for 2 BHK apartments is Rs. 50 Lakhs, you should not consider opting for a Mutual fund which would become Rs.50 Lakhs after 8 years. Because the price of the apartment can change within that 8 year span significantly and you should estimate an approximate value it would have at a future date by taking into account inflation and other economic considerations along with a safety margin. At the bare minimum, you should consider opting for a Mutual Fund Scheme of 8 years which on redemption can give you at least Rs. 70 Lakhs. So we intended to mention here is that the Amount you considered should be adjusted with the time period within which you plan to achieve the goal.

So Now you know the Amount of Money you require to achieve your goal and the Time period defined by you for the same. Historic data of Mutual Fund performance shows that if you plan to meet a Financial goal within 3 years of time, Debt type mutual Funds are the best suited as they will give consistent and safe returns. And debt mutual fund performance usually outperforms Equity Mutual funds if the investment horizon is ranging from 2 Days to 2 years.

If you plan to achieve your goal in 5 years or 10 years time frame, In such a case equity-based Mutual Funds will be the ones that could provide higher returns, if you are willing to take that extra risk. It’s worth noting that Equity funds on a long term of 10+ years can give you much higher returns compared to Debt Funds due to their higher growth potential.

One more interesting thing to note while investing in Equity Funds for long term is, Suppose your child’s marriage is expected to be in 8 years and decide to have an Equity-based mutual fund, In that case, you should not opt for an Equity Scheme of 8 years instead go with an Equity scheme for 7 years and on the last 1 year go with a debt plan. It is advised in such a way because imagine if you have gone with an Equity-based Plan for a whole 8 years and the market crashes on the 8 year, in that case, you won’t be getting the planned amount due to a sudden crash on market. That 1 year is a safe margin suggested if your long term goal is of supreme importance which you could not afford to miss at any cost, in such cases, you should redeem the Equity Mutual Fund 2 years prior to the planned date of achieving your goal and invest the whole into a Good Debt Mutual Fund with high liquidity for the last 2 years, in such a way you have enjoyed the benefits of having Equity Mutual Fund for the long term and Intelligently Ensured the safety of the wealth you grown by keeping it readily available in a Debt Fund during your Future moment. We have seen that even after the Global 2008 crash and 2021 crash, the Equity market has recovered within 2 years span, that is why the 2-year safety margin on time frame is suggested.

For short Duration Plans within 2 years, you could choose anyone among the best Liquid Fund, Ultra short term Fund or any such type of Debt Funds which gives better returns and have low expense ratio from a trusted and credible Fund House.

The below Checklist will help you to achieve the best suitable Mutual Fund schemes available in the market that suit you the best,

- Check Your Risk Profile : Decide your risk appetite

- Selection of Fund Category : Based on Risk appetite and Goal choose whether to go with Equity / Debt / Hybrid Funds

- Selection of Fund Sub Category : Based on your goal, risk, investment horizon rule out fund types which you are not interested

- AUM : Check for Schemes which has highest AUM, high AUM funds usually have low Expense ratio and it shows confidence of a larger community on the Fund

- Performance Analysis : Analyse the past performance and consistency of the returns provided by the group of funds shortlisted based on above criterias. Always check the consistency of returns provided by the Fund on a yearly basis.

- Selection of Fund House : Choose a group of Trusted, Reputed and Credible Fund House familiar to you and on which you are confident.

- Age of Fund : Choose Funds which are in the market at least for 5 years, so that we could have a better comparison of the performance.

- Analyse the Expense Ratio ; Schemes with low expense ratio are often better.

- Sectoral allocation : From the shortlisted Schemes find those which invest in sectors which you believe has great growth potential in future.

- Fund Manager : Check the Fund Manager profile, experience and his duration he managed the Fund.

- Portfolio Analysis : Check the Portfolio of assets invested by the Fund and decide whether it matches your market perspective.

- Riskometer : Find the Riskometer value of the Fund from the Fund sheet and choose one with low risk or based on your risk appetite.

The above checklist and criteria will help you to trim down from a huge list of Mutual Fund schemes to a narrow list, from which you could easily select a suitable Mutual Fund Plan. Nowadays multiple apps and screeners are available which will help you to shortlist the Mutual Funds quickly and will ease your selection process.

Always remember to choose a Mutual Fund which matches your risk appetite and will grow your wealth as per your financial goals, aligning with your market and economic perspective which will give you confidence and help you to achieve Financial Freedom. Good Luck and Best wishes….!!!

Types of Investment Options in Mutual Fund

Congratulations…!!! You have reached the final part of our Mutual Fund series and we are pretty much confident that now you have a much better awareness and knowledge about the Mutual Funds in our Country and are familiar with the key things about it. You have to visit some of the leading apps or websites which offer Mutual Fund services to realize the great value of the knowledge you have, now you will be in a better position to identify multiple schemes, make good comparisons and pick the best one for you.

In this final article, we would like to point out the types of investment options available in Mutual Funds, most of you might be familiar with them but let’s have a quick glimpse of them.

- Lump Sum

Certain Funds like Closed-ended funds and a few Debt Funds mandates Lump sum investment. It means you have to make a Fixed One time Investment when you join the mutual fund scheme and let the investment grow for the time period specified.

- Systematic Withdrawal Plan (SWP)

In this mode of Investment scheme, you will have to invest a fixed lump sum amount at the beginning of the Mutual Fund and you could withdraw periodically a certain amount, like monthly, and the rest of the investment continues with the plan till it gets completely settled. Your invested Capital grows as per policy returns and you could have regular withdrawals in this scheme. These are best suited for retired people, who will have a lump sum amount in hand while retiring which they could invest for better returns and also take out a certain portion of it monthly to meet living expenses.

- Systematic Investment Plan (SIP)

This is one of the most popular and best-suited investment options for the general salaried public who could not make a Lump sum investment in the Mutual Funds. Most of the Mutual Fund schemes provide the facility to make SIP mode of investment. Here the investor could make a predefined periodic investment on the mutual Fund Scheme he chooses, like making investments monthly, quarterly etc.

As we discussed in the previous chapter you have decided the Amount of Money and Time period within which you aim to achieve a life goal. You just have to input these data along with the frequency of investment (Monthly, Quarterly, Yearly etc) into the SIP calculator and it will show you the monthly (Periodic) investment you have to make so as to achieve your future goal.

This is one of the best suited and popular modes of investment in Mutual Funds for regular income people which facilitate them to achieve their long-term financial goals by making regular affordable periodic investments. If you opt for a SIP mode the periodic Investment directly gets debited from your bank account on the date you specify and makes your investment process in the Mutual Funds even simpler. (The automated debiting Facility from savings account into Mutual Funds directly is supposed to be discontinued from Financial Year 2022-2023 as per RBI Guidelines, after which you will be required to provide an OTP-based approval to withdraw money from your account to make such monthly investments).

There are multiple subtypes of SIP and are,

- Flexible SIP – Here you could vary the monthly installment amount within a range specified in the Mutual Fund Scheme

- Step Up SIP – Which allows the Investor to Increase the periodic Installment amount after a certain period, usually after 1 continuous year of investment in the Fund

- Trigger SIP – Where you could specify a particular NAV value to be considered as an Entry point on the Mutual Fund Scheme. Just like Limit order in Stocks.

- Pause SIP – It allows you to pause the periodic installments for a short duration if you undergo any crisis like job loss, accident etc.

All Mutual Fund schemes will not give you the option to choose the subcategory modes of SIP, so the Scheme Information Document should clearly read to understand the terms and condition of the Mutual Fund Scheme and the flexibility of Investment modes it provides.

One Additional benefit of Choosing the SIP mode of Investment in Equity-based Mutual Funds is that as you are making periodic investments in the Fund you are getting the benefit of averaging effect on your portfolio. Some months you will be making the investment when markets are at peak and some other months you are making an investment when markets are down, so In Equity-based SIP investment, you are getting the averaging effect as a bonus , which can give you a better return of Investment.

4. Systematic Transfer Plan (STP)

An STP is a plan that allows investors to give consent to a mutual fund to periodically transfer a certain amount / switch certain units from one scheme and invest in another scheme of the same mutual fund house. Thus at regular intervals, an amount/number of units you choose is transferred from one mutual fund scheme to another of your choice. For Example, STP Facility allows you to invest in Equity Funds if you feel it is booming and could switch the funds to a Debt Fund if you feel the equity market can go bearish.

So that marks the End of the Amazing Mutual Fund Series, which we strongly believe helped you to give more insightful and in-depth knowledge on Mutual Funds that could help you to make intelligent decisions while you plan to invest in a Mutual Fund by yourself …..!!!

Leave a Reply